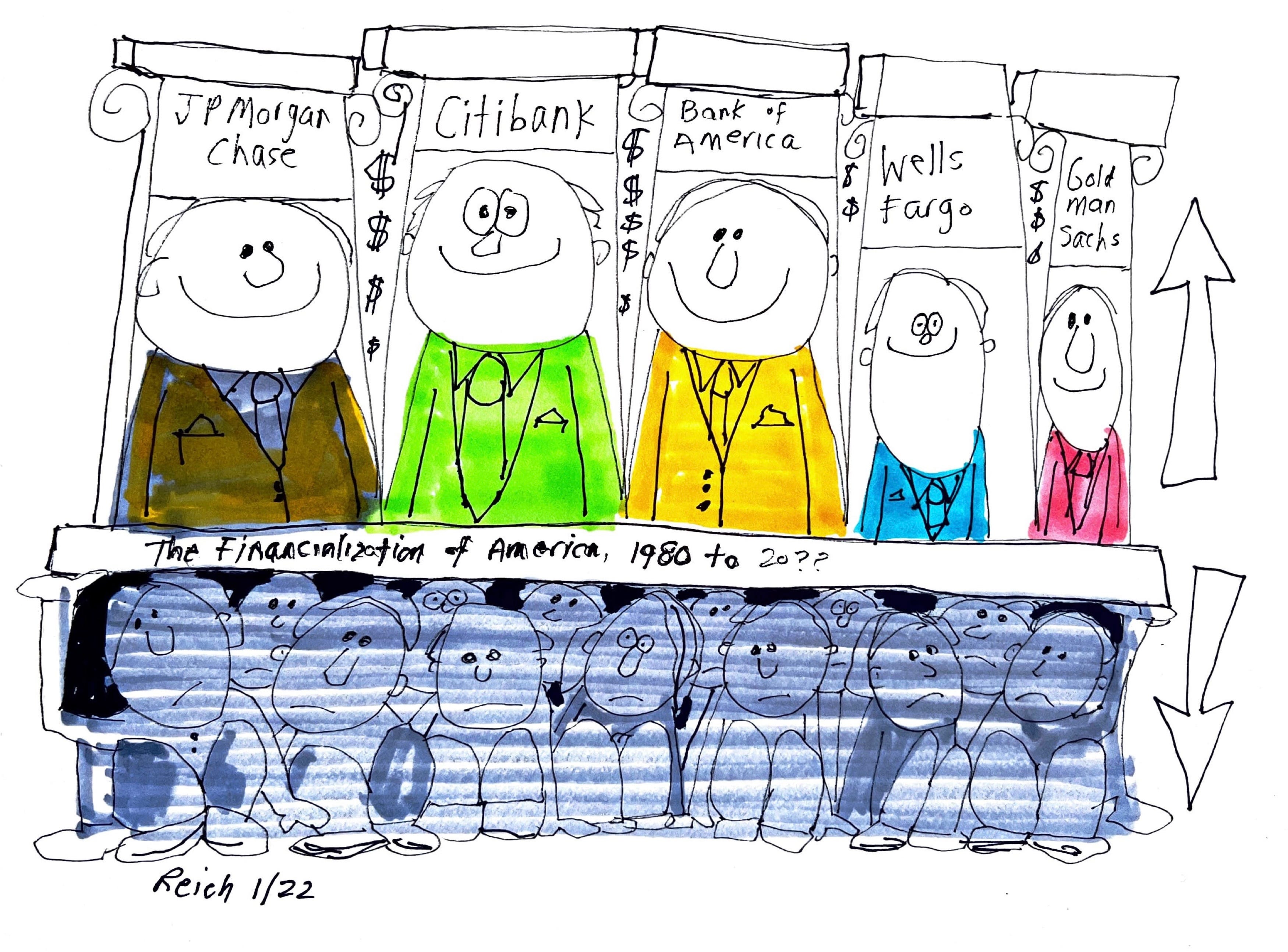

Wall Street may be having a bad week, but top bankers are doing wonderfully well. After a blockbuster year, the five biggest Wall Street banks just paid out $142 billion in bonuses and compensation for 2021. This was $18 billion more than in 2020. JPMorgan Chase reported record profits, and Citigroup’s annual profit more than doubled. Let me remind you (as if you need reminding) that 2020 and 2021 were not exactly blockbuster years for the rest of America.

In the first three decades after World War II, American companies made money by making things, selling them at a profit, and investing the profits in additional productive capacity. This helped create the largest middle class the world had ever seen. In those years, the financial sector accounted for 15 percent of U.S. corporate profits.

Then something happened. By the mid-1980s, the financial sector claimed 30 percent of corporate profits. By 2001, 40 percent — more than four times the profits made in all U.S. manufacturing.

Why this dramatic change? Indulge me a moment as I quote from a New York Times op-ed I wrote more than forty years ago (May 23, 1980):

The paper entrepreneurs are winning out over the product entrepreneurs.

Paper entrepreneurs – trained in law, finance, accountancy – manipulate complex systems of rules and numbers. They innovate by using the systems in novel ways: establishing joint ventures, consortiums, holding companies, mutual funds; finding companies to acquire, “white knights” to be acquired by, commodity futures to invest in, tax shelters to hide in; engaging in proxy fights, tender offers, antitrust suits, stock splits, spinoffs, divestitures; buying and selling notes, bonds, convertible debentures, sinking-fund debentures; obtaining government subsidies, loan guarantees, tax breaks, contracts, licenses, quotas, price supports, bailouts; going private, going public, going bankrupt.

Product entrepreneurs – engineers, inventors, production managers, marketers, owners of small businesses – produce goods and services people want. They innovate by creating better products at less cost.

Our economic system needs both. Paper entrepreneurs ensure that capital is allocated efficiently among product entrepreneurs. But paper entrepreneurs do not directly enlarge the economic pie. They only arrange and divide the slices. They provide nothing of tangible use. For an economy to maintain its health, entrepreneurial rewards should flow primarily to product, not paper.

Yet paper entrepreneurialism is on the rise. It dominates the leadership of our largest corporations. It guides government departments, legislatures, agencies, public utilities. It stimulates platoons of lawyers and financiers.

It preoccupies some of our best minds, attracts some of our most talented graduates, embodies some of our most creative and original thinking, spurs some of our most energetic wheeling and dealing. Paper entrepreneurialism also promises the best financial rewards, the highest social status.

The ratio of paper entrepreneurialism to product entrepreneurialism in our economy – measured by total earnings flowing to each, or by the amount of news in business journals and newspapers typically devoted to each – is about 2 to 1.

Why? Our economic system has become so complex and interdependent that capital must be allocated according to symbols of productivity rather than according to productivity itself. These symbolic rules and numbers lend themselves to profitable manipulation far more readily than do the underlying processes of production.

It takes time and effort to improve product quality, exploit manufacturing efficiencies, develop distribution and sales networks. But through strategic use of accounting conventions, tax rules, stock and commodity exchanges, exchange rates, government largesse, and litigation, enormous profits are possible with relatively little effort.

When paper entrepreneurs look for solutions to America’s declining productivity and international competitiveness, they come up with paper remedies to stimulate large-scale capital investment: accelerated depreciation, tax credits, government subsidies, relaxation of antitrust laws.

Product entrepreneurs focus on techniques for improving output: better quality controls, improved labor-management relations, more effective incentives for managers and employees, more aggressive marketing and sales.

If we are to increase the economic pie, we will need to redress the balance of entrepreneurial effort. Which strategies will stimulate more paper, and which more product?

I wish I had not been as prescient. Yet the dominance of finance over much of the American economy since 1980 didn’t happen by accident. It needed the help of politicians — including presidents (both Republican and Democrat) — who changed laws and regulations to encourage it.

Ronald Reagan’s Securities and Exchange Commission allowed corporate raiders to use borrowed money to buy and dismantle American companies. The raiders (now more politely called “private-equity” managers) sold off divisions, squeezed costs, and fired workers—all to maximize “shareholder value.” The result may have been “efficient” in the narrowest sense of the term but it was socially disastrous. Manufacturing employment plummeted. Unions died. Great swaths of the Midwest and South were abandoned. Men without high school degrees suffered knockout blows. The typical wage — which had been rising steadily since the end of World War II, in tandem with the increasing productivity of the nation — began to stagnate (adjusted for inflation). For men without college degrees, real wages started a long decline.

It wasn’t just Reagan. Bill Clinton (with the advice of Robert Rubin and Lawrence Summers) opened the door to more financial speculation by refusing to regulate highly-leveraged derivatives (the opaque, highly profitable instruments of financial speculation that Warren Buffet called “financial weapons of mass destruction”) and by supporting Republican efforts in Congress to repeal the Glass-Steagall Act (the Depression-era law that required the separation of commercial and investment banking) and allow the creation of megabanks.

When the financial bubble inevitably burst, Barack Obama endorsed the Bush administration’s Wall Street bailout and appointed many of the same team of Clinton-era economic advisors who, while working under Rubin in the 1990s, had laid the groundwork for the financial crisis by encouraging speculation. Obama did what they then recommended: restore the profitability of Wall Street banks rather than reduce the power of finance and help millions of Americans who lost their homes.

The bailout of Wall Street came without strings. The Obama administration did not fire any Wall Street CEOs. It did not rein in their egregious pay. It did not prevent the big banks from buying back their stock or handing out generous dividend payments to their stockholders. It imposed no losses on the banks’ shareholders and creditors. It did not insist that banks stop their lobbying to obstruct reform the financial industry. Instead, Obama (and his economic advisors, headed by Laurence Summers) shifted the costs of Wall Street’s speculative binge onto ordinary Americans -- deepening public mistrust of a political system increasingly seen as rigged in favor of the rich and powerful.

A direct line runs from public anger over the bailout of Wall Street to the Occupy movement and the candidacy of Bernie Sanders, on the left; and to the Tea Party movement and the election of Donald Trump, on the right.

I saw it and heard it in early 2016 in Michigan, Wisconsin, North Carolina, Ohio, and Iowa where I conducted focus groups: Whenever I mentioned the establishment presidential candidates Jeb Bush or Hillary Clinton, people told me they didn’t stand a chance. Instead, the people I interviewed were excited by Bernie Sanders or Donald Trump. (A remarkable number said they supported both.)

Again and again, I heard references to the bailout of Wall Street as proof that the economy was “rigged” against ordinary Americans, and that America needed a president who would champion average working people. As Americans went to the polls later that year, 75 per cent said they were looking for a leader who would “take the country back from the rich and powerful.” They obviously didn’t get one. Trump masqueraded as a tribune of the working class but was a Trojan horse for the rich and powerful.

We are still living with the political and social consequences of America’s turn to financial entrepreneurship. The five biggest Wall Street banks could not have scored record profits these past two years were they not back to many of the same practices that caused them to implode in 2008 and the rest of America to pay the price. Inequalities of income and wealth are far wider now than they were when Wall Street’s bubble burst. I suspect even more Americans today feel the system is rigged by the rich and powerful than they did a few years ago.

It doesn’t have to remain this way. We are not prisoners of bad decisions made in the past. We can and should rein in Wall Street, break up its five giant “too-big-to-fail” banks, support local and state banks, resurrect the Glass-Steagall Act’s divide between investment and commercial banking, tax all financial transactions — and rebuild jobs and wages on the product side of the American economy.

Share this post